The Formation Paradox

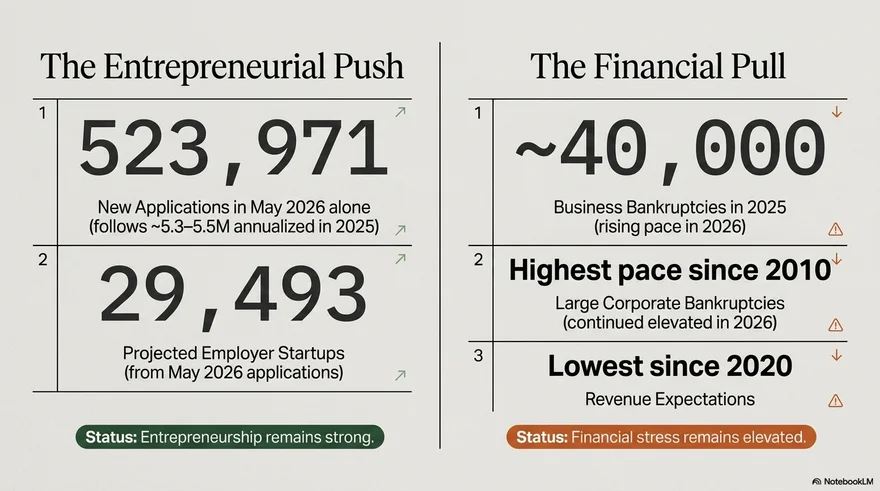

The raw entrepreneurial energy in the United States remains extraordinary. Nearly 524,000 new business applications in a single month is not a number that belongs in a recession narrative. Roughly 29,500 of those are projected to become employer businesses within a year — actual firms that hire people, lease space, and generate payroll. By any historical standard, this is a remarkable rate of formation.

But formation alone is a misleading indicator of economic health. The question that matters is not how many businesses Americans are willing to start, but how many of those businesses can survive long enough to matter. And here the data turns grim. Approximately 40,000 business bankruptcy filings in 2025, with the pace still climbing into 2026. Large corporate bankruptcies hit their highest rate since 2010, concentrated among firms carrying debt loads that made sense in a different interest-rate era but have become unsustainable in this one.

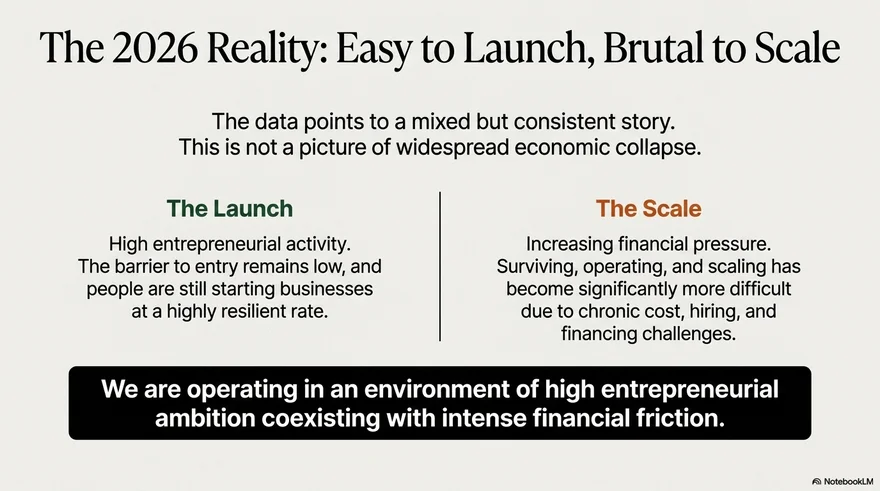

What emerges is not the familiar picture of a healthy economy generating confident new ventures. It is something stranger and more unsettling: an economy where starting a business has never been easier and surviving as one has rarely been harder. The barriers to entry have dropped — digital tools, remote work infrastructure, and streamlined registration processes all contribute — while the barriers to continuation have risen sharply. The result is an entrepreneurial landscape that functions less like a garden and more like a rapids, with an enormous volume of activity moving through a channel that very few navigate intact.

The Pincer: Squeezed From Both Sides

To understand why survival has become so difficult, look at the financial architecture surrounding a typical small business in mid-2026. It faces what might be called a pincer movement — simultaneous pressure from rising costs on one side and contracting capital access on the other.

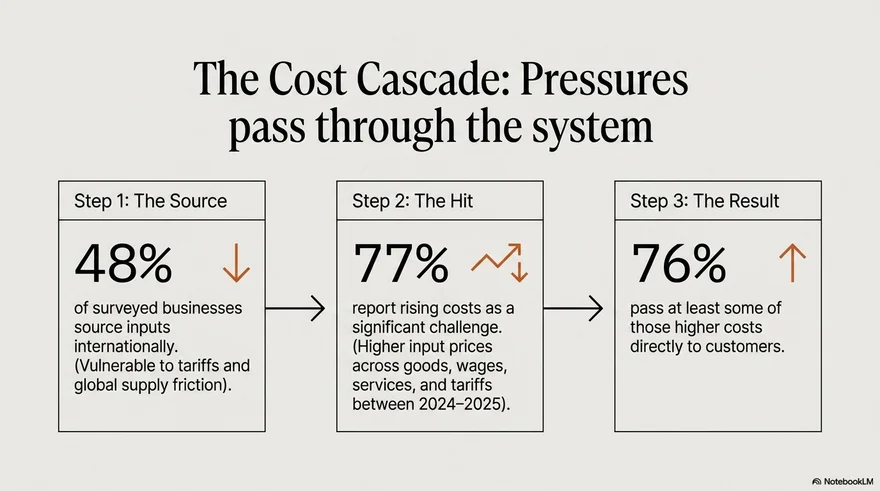

On the cost side, the pressure is nearly universal. More than three-quarters of employer firms report rising expenses across a broad front: goods, wages, services, and tariffs. This is not a single-variable problem that can be solved by switching suppliers or renegotiating a lease. It is a systemic increase in the cost of doing business, touching every line item on the income statement more or less at once. And for the nearly half of firms that source inputs internationally, tariff exposure adds an additional layer of volatility that is entirely outside their control.

The natural response — passing costs through to customers — has been widespread, with 76% of firms reporting they have raised prices to some degree. But this strategy has a ceiling, and many businesses are approaching it. Weakening customer demand is now cited alongside inflation and labor costs as a primary concern. The very mechanism businesses are using to survive the cost squeeze is contributing to the demand squeeze. It is a feedback loop with diminishing returns.

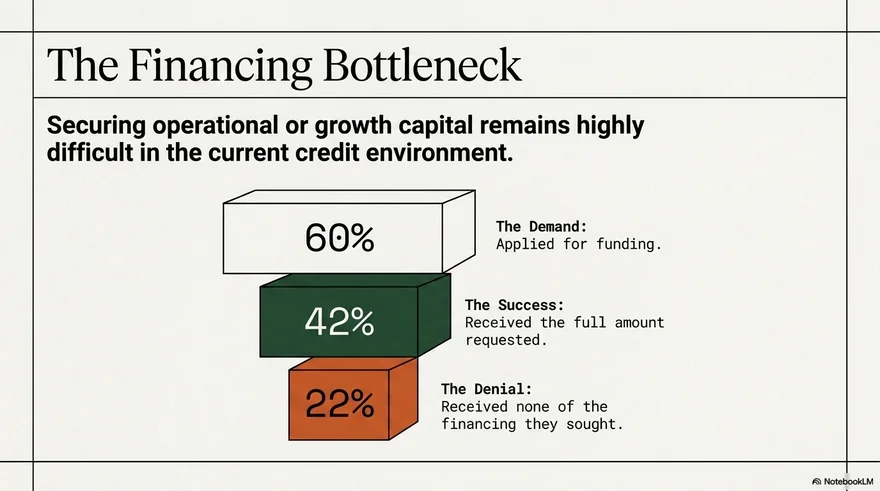

On the capital side, the situation is arguably worse. Sixty percent of businesses sought funding in the current environment — these are firms that need external capital to bridge gaps, cover rising costs, or simply keep operating. Of that group, fewer than half received what they asked for. More than one in five received nothing at all. This is not a story about expensive money. It is a story about absent money. The credit market has shifted from charging more to simply saying no.

For a business caught between costs it cannot cut and capital it cannot access, the mathematics of survival become very tight very quickly. The margin for error — a slow month, an unexpected expense, a delayed receivable — shrinks to almost nothing. And when there is no margin for error, errors become fatal.

The Sentiment Collapse

Numbers on a spreadsheet are one thing. The psychology of the people behind those numbers is another, and in 2026, that psychology has shifted decisively toward caution.

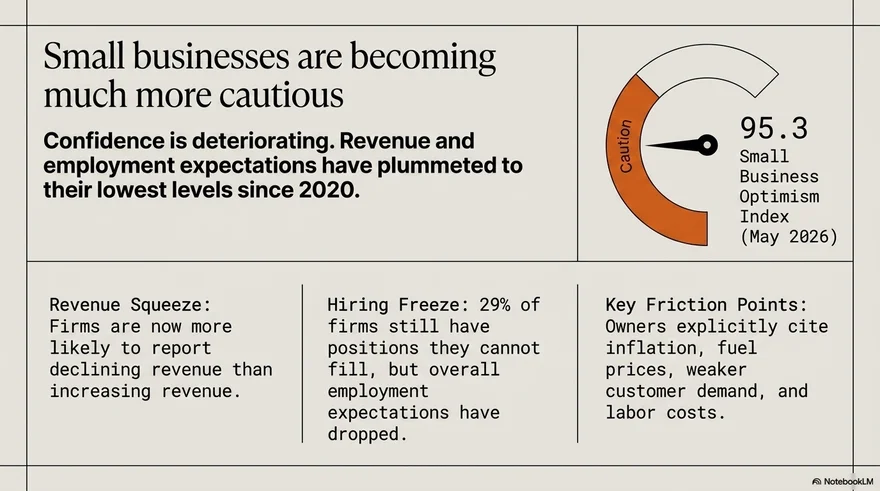

Revenue growth expectations and employment outlooks have fallen to their lowest levels since 2020 — a comparison that should land with some force, given what was happening in 2020. The Small Business Optimism Index sits at 95.3, a number that reflects not panic but a grinding, pervasive anxiety. Business owners are not predicting disaster. They are simply no longer predicting improvement.

This matters because small business behavior is deeply responsive to sentiment. An owner who expects growth hires ahead of demand, invests in equipment, and takes on prudent debt. An owner who expects stagnation or contraction does the opposite: delays hiring, defers maintenance, hoards cash, cuts discretionary spending. When this defensive posture becomes widespread — and the data suggests it has — it becomes self-reinforcing. Caution reduces spending, which reduces someone else's revenue, which increases their caution in turn. The macroeconomic term for this is a paradox of thrift. The small business term for it is Tuesday.

What is particularly striking is that firms are now more likely to report declining revenue than increasing revenue. This is not a projection or a fear. It is a present-tense reality that a plurality of businesses are already living inside.

The Structural Traps

If the cost-credit pincer and the sentiment collapse were the only problems, they might be cyclical — painful but temporary, the kind of downturn that recedes when rates fall or consumer confidence returns. But the 2026 data reveals structural issues that will persist regardless of where the business cycle turns next.

The labor market remains stubbornly misaligned with small business needs. Twenty-nine percent of firms report positions they cannot fill, a number that has barely moved even as optimism has cratered. This is not a wage problem that can be solved by offering more money — if it were, the same cost pressures forcing prices up would also be clearing the labor market. It is a skills mismatch, a geographic mismatch, or both. The workers who are available are not the workers these businesses need, and the workers these businesses need are either not available or not available at a price point that the business can sustain.

Meanwhile, the refinancing cliff looming over leveraged firms represents a slow-motion structural adjustment that will play out over years. Businesses that took on debt when rates were near zero are now facing renewal at dramatically higher rates. For firms with strong cash flows, this is an inconvenience. For firms that were viable only because their debt service was cheap, it is an existential threat. The concentration of large corporate bankruptcies among highly leveraged companies is the leading edge of this wave, not the whole of it.

What the Churn Economy Means for Founders

The temptation, when presented with data this mixed, is to reach for a simple verdict. The economy is either fundamentally strong (look at those formation numbers) or fundamentally weak (look at those bankruptcy numbers). But the more honest reading is that neither frame captures what is actually happening.

What the 2026 data describes is an economy in a state of accelerated metabolic activity. Old firms — particularly those built on assumptions about cheap capital, stable supply chains, and predictable demand — are failing at an elevated rate. New firms, often smaller, leaner, and more digitally native, are forming at an extraordinary pace to fill the gaps they leave behind. The net effect is an economy that is simultaneously vigorous and fragile, dynamic and precarious.

This has profound implications for the people inside it. For workers, it means that the employer they join today may not exist in two years — not because the economy collapsed, but because the normal rate of business turnover has accelerated. For entrepreneurs, it means that the window between launch and viability has narrowed. There is less time and less capital available to find product-market fit before the pincer closes. For policymakers, it means that traditional indicators of economic health, designed to measure expansion or contraction, are poorly suited to measuring an economy whose defining characteristic is velocity.

The 523,971 applications filed in a single month in May 2026 are not a sign that everything is fine. The 40,000 bankruptcies are not a sign that everything is broken. They are, taken together, the vital signs of an economy that has entered a new and unfamiliar phase — one defined not by the direction of change but by its speed. The question is no longer whether America's small business sector is growing or shrinking. It is whether the rate of churn has crossed the threshold at which it stops being creative destruction and starts being just destruction.

That threshold, if it exists, is not visible in the current data. But neither is the evidence that we are safely below it.

Further reading

Score your own PMF in 20 minutes.

Free PMF score across market, founder, and execution readiness — with named blind spots and specific first actions. No credit card required.